When to Register a Firm

The following flowchart best illustrates the requirements for firm registration and licensure:

A member, or group of members, shall register a firm prior to providing the following specific services:

A firm is deemed to be providing services in Saskatchewan when:

- A member is practicing professional accounting or other regulated services to a client;

- A client is a resident of Saskatchewan; or

- The client’s books and records are substantially located in Saskatchewan

The service to the public can be in one or both forms:

1. A member of a firm practicing professional accounting must have a licence. The practice of professional accounting (defined in Section 18 of the Act) consists of:

- Audit engagements

- Other Assurance engagements, including Review Engagements

- Providing Financial Reporting advice which references the CPA Canada Handbook

- Compilation engagements

2. Other regulated services consists of:

- accounting services;

- bankruptcy and insolvency trusteeship or administration;

- engagement quality control reviews;

- finance services;

- forensic accounting;

- management accounting; and

- taxation services;

and does not include the practice of professional accounting.

Penalties

Board Rule 472.1 A member who practices professional accounting without being licensed under Section 18(2) of the Act shall be charged a penalty as set by the Board.

Board Rule 472.2 A member who practices professional accounting or other regulated services without notifying the Institute prior to commencement of practice shall be charged a penalty as set by the Board.

Definitions:

“accounting services” means analysis, interpretation, advice or counsel related to financial information or a financial reporting standard contained in or applicable to general purpose financial statements and does not include:

1. the practice of professional accounting;

2. management accounting; or

3. bookkeeping.

“taxation service” means providing advice or interpretation with respect to taxation matters.

“client” means a person, other than the member’s employer, who in the view of a reasonable observer enters into or places reliance on a relationship or engagement for professional services with a member or firm.

“management accounting” means identifying management information requirements and developing the required systems and includes:

1. planning;

2. forecasting;

3. budgeting;

4. management reporting;

5. cost and revenue management; and

6. analysis or advice with respect to the foregoing.

"finance services" means providing advice related to treasury management, capital budgeting, business valuation or corporate finance transactions.

Do I need to register if I prepare tax returns?

For clarity, there is a difference between tax preparation and tax advice. There are limited circumstances where completion of a tax return by a Chartered Professional Accountant (CPA) would be seen as preparation. There is a presumption that the public would seek the services of a CPA for his or her professional judgment and expert knowledge of the Income Tax Act (ITA), therefore the preparation of corporate (T2) and trust (T3) returns are considered to be providing services to the public in some cases.

The preparer of a corporate return, for instance, requires an understanding of financial statements and the ITA to identify information to include on the return, therefore would likely be providing tax advice.

In the context of a personal tax return (T1), preparation could be limited to inputting a few tax slips and performing very simple calculations. If there are choices to be made requiring the exercise of professional judgment and tax knowledge, such as which spouse should deduct donations or RRSP contributions on their respective T1 returns to realize the maximum benefit, the member is providing advice in an expert capacity and is therefore engaged in providing other regulated services.

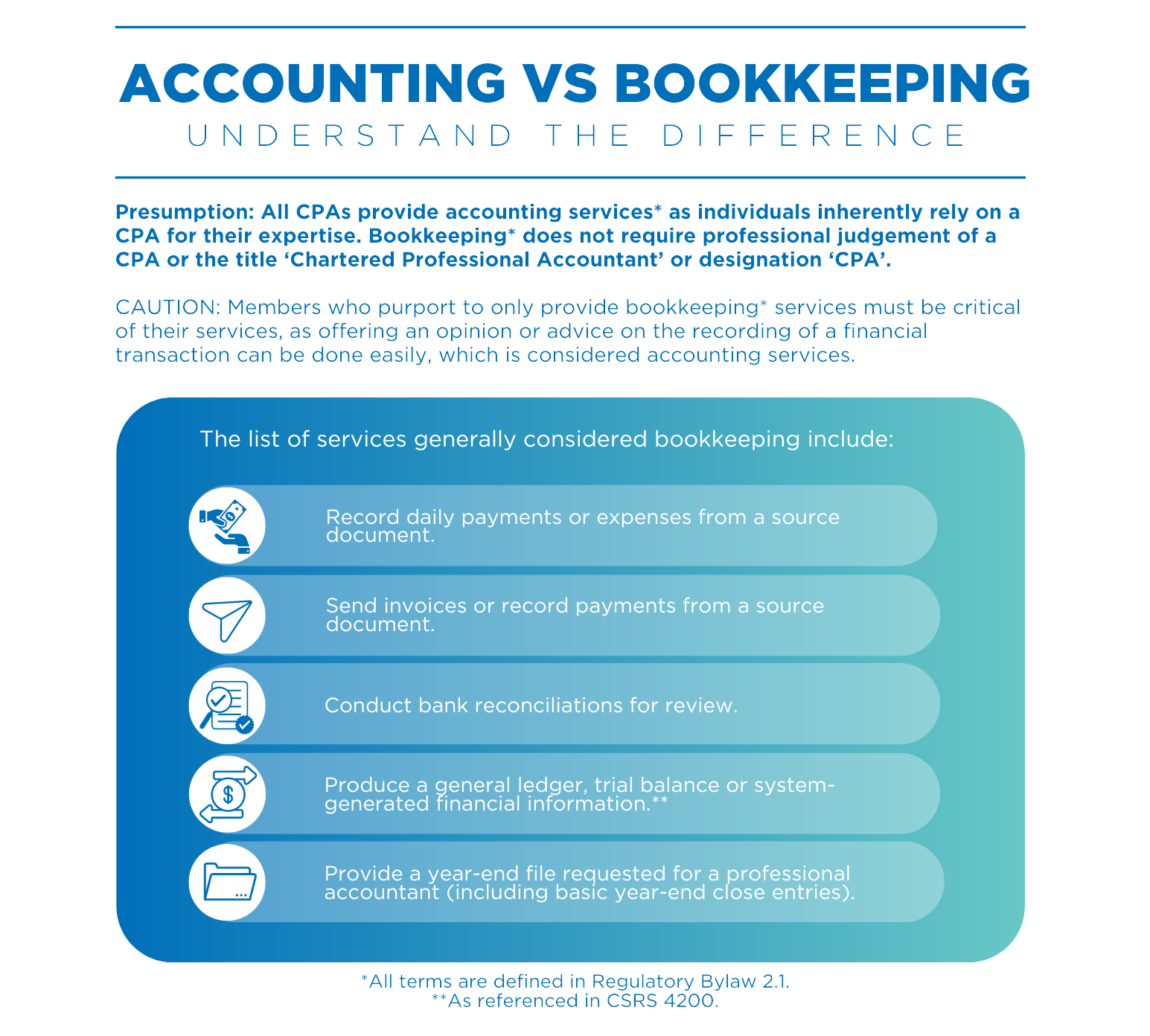

Do I need to register if I provide bookkeeping services?

Bookkeeping is not a service which requires registration of a firm. Bookkeeping is defined as, “the preparation or maintenance of an entity’s accounting records including a trial balance and reports produced directly from such records.”

The preparation of financial statements becomes less clear if the member is using software to get to a trial balance. If the financial statements are output of the work performed to get to the trial balance, it is likely a bookkeeping function. Additional analysis on the financial statements may be considered management accounting and therefore other regulated services. Further, providing an opinion on the compliance of the financial statements with a stated basis of accounting published in the CPA Canada Handbook shall require a licence.

When did Consulting require the need to register a firm?

Since 2014, CPAs who offer management accounting services to the public are required to register a firm.

Management Consulting may often be referred to as Management Accounting, which is a regulated service.

Management accounting encompasses a range of services, including budgeting and forecasting, cost management, performance measurement, financial analysis, and the integration of digital technologies.

These services directly support decision-making within organizations. CPAs specializing in management accounting provide essential insights that guide day-to-day operations, assist in long-term strategic planning, and enable businesses to optimize resource allocation, manage costs effectively, and measure progress against financial and strategic goals.

The technical competency of management accounting equips CPAs with the skills needed to interpret complex financial date; helping businesses navigate market conditions and internal challenges. The integration of digital technologies into management accounting practices also allows CPAs to leverage data analytics, machine learning, and artificial intelligence, enhancing their ability to provide innovative solutions that drive business success.

By leveraging competency in management accounting, CPAs are relied on to provide a vital role in shaping the financial health and strategic direction of the organization.

Professional Liability Insurance

Firms must have professional liability insurance under Regulatory Bylaw 24.1. For firms engaged in the practice of professional accounting, compilation engagements or taxation services, the following are the minimum requirements based on Rule 324:

- $1,000,000, where one (1) member is engaged or employed in one or both of the practice of professional accounting or other regulated services in the same firm;

- $1,500,000, where two (2) or three (3) members are engaged or employed in one or both of the practice of professional accounting or other regulated services in the same firm; or

- $2,000,000, where four (4) or more members are engaged or employed one or both of the practice of professional accounting or other regulated services in the same firm.

The minimum requirements for professional liability insurance specified in Board Rule 324.1 per occurrence and in aggregate and coverage for defense costs shall be in addition to the specified minimum requirements.

Further to Bylaw 24.2, every firm shall provide to the institute a certificate of professional liability insurance coverage within thirty (30) days from commencement of practice or the anniversary date of the policy.

Some common preferred providers that are familiar with the CPA requirements are: CPA Professional Liability Plan Inc., PROLINK Insurance. Use your professional judgement when selecting a provider that is not familiar with the provisions required by CPA Saskatchewan. You may not be getting the coverage you need.

Professional Corporation

Any member who practices the profession in corporate form shall register as a professional corporation. A professional corporation is subject to the provisions of The Professional Corporations Act and is one type of entity included in firms. The name of a professional corporation must include “CPA” or “Chartered Professional Accountant” and "Professional Corporation", "Prof. Corp.", "P.C. Inc.", or "P.C. Ltd." You will need to complete the filing with the Corporate Registry (Information Services Corporation of Saskatchewan) and the registration with CPA SK.

Exemptions

Bylaw 14.2 Subject to Bylaw 14.3, a member providing other regulated services qualifies for an exemption from registration of a firm when the professional service provided is:

(a) to three (3) or fewer clients;

(b) as an officer or director in a volunteer capacity;

(c) to or through a registered firm; or

(d) governed by another professional regulatory body established pursuant to legislation in Saskatchewan.

Bylaw 14.3 A member shall submit a declaration regarding his eligibility for exemption under Bylaw 14.2 in the form approved by the applicable regulatory committee which shall indicate:

(a) the subclause in Bylaw 14.2 which applies; and

(b) his professional services are not advertised, marketed or otherwise promoted to the public other than by an application for employment.

A member shall submit a declaration regarding eligibility for exemption (or as a change occurs). We require a written submission by email to keep in your file. If you have more than 3 clients in Saskatchewan, then you will be required to register a firm.

Next Steps

The first step is to obtain approval of the preferred firm name. Please email your preferred firm name to the Registrar. Once the firm name has been approved, the required registration applications will be sent to you. In addition to the annual membership renewal on April 1, firm and/or professional corporations are renewed annually with an expiry date of December 31. Renewal starts November 1.