Licensing Requirements - Member and Firm

In addition to member registration, a licence with CPA Saskatchewan is required for those members looking to execute audit, review, other assurance, or compilation engagement reports. This is referred to as practicing professional accounting.

![]()

What is practicing professional accounting?

The practice of professional accounting is a reserved area of practice to licensed CPAs only under subsection 18(1) of The Accounting Profession Act (the Act). The practice of professional accounting includes the following services to or for the benefit of a client in accordance with the Standards of Professional Practice set out in the CPA Canada Handbook:

- Audit engagements of historical financial statements or financial information

- Review engagements of historical financial statements or financial information

- Other assurance engagements

- Compilation engagements on financial information

- Financial reporting opinions, certifications, declarations, or agreed-upon procedures

The Act provides for limited exemptions from the requirement to hold a licence to practice professional accounting in subsection 18(3). If a non-member or member is relying on an exemption under the Act, they must complete a required form and include supporting documentation for that exemption or be subject to a cease-and-desist order issued by the Registrar.

Who requires a licence?

Not all members at a firm need to obtain a licence; only the member(s) given the authority on behalf of a firm to authorize the release of assurance or compilation engagement reports or financial reporting opinions, declarations or certifications is (are) required to be licensed. Members assigned to an assurance or compilation engagement team who do not have responsibility for the final approval and issuance of the engagement report are not required to be licensed. For planning or staff transition purposes, a member may choose to make an application, provided they have authority to act on behalf of the firm.

For more information about whether the type of services provided to the public require licensure and firm registration, see When to Register a Firm.

A firm licence is issued when at least one member of the firm becomes licensed. In the case of a firm with more than one licensed member, the firm is issued a licence based on the member who holds the highest-level licence.

A member must be employed at a registered firm and must apply and be approved for a licence prior to offering any type of professional accounting services to or for the benefit of a client, including any member practicing within another jurisdiction in Canada (see more details about affiliate licensing below).

Any member practising professional accounting without a licence is subject to penalty of $1,000 per report issued, up to $3,000. Continued non-compliance may include escalating consequences through the cease-and-desist process and may include the consideration of a professional conduct complaint.

Public Access to Licensing Information

The licensing status of a member and a firm is publicly available information. Members of the general public, employers, or others can access this information at any time through our online directories at: Find a CPA Member and Find a CPA Firm .

The directory will indicate the type of licence held by the member or firm, if applicable.

Affiliate Members Practicing Professional Accounting in Saskatchewan (Labour Mobility Licensure)

Affiliate members who practice mainly in another provincial jurisdiction but are seeking assurance or compilation clients located in Saskatchewan (or who wish to execute a report from a Saskatchewan location) must first obtain affiliate membership (if not already), register an affiliate firm (if not already) and submit a licence application prior to offering these services in Saskatchewan.

The affiliate member is issued an equivalent licence to what they currently hold in their primary jurisdiction upon review and confirmation of information within the required application form. The applicant member and their firm must be in good standing within their primary provincial jurisdiction, and they must already be authorized in the applicable area of practice in their primary jurisdiction to qualify for a licence in Saskatchewan. This means that the applicant cannot apply for a higher licence tier than what they are currently authorized for in their primary jurisdiction nor can they seek to become a primary member in Saskatchewan to qualify for a higher licence tier, even if they meet all applicable minimum requirements outlined below. The applicant would be required to seek this higher tier of licensure in their primary jurisdiction first, before making an application in Saskatchewan. Any conditions or restrictions on the applicant member or firm in the primary jurisdiction will also be reflected on the Saskatchewan licence. Contact licensing to obtain more information about the licensing application process and applicable forms.

Types of Licences

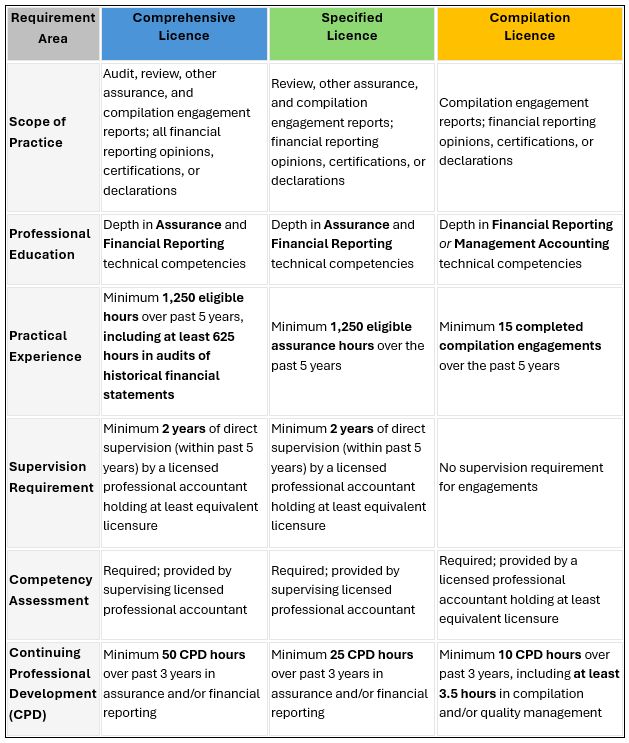

Comprehensive Licence: A comprehensive licence allows the member to complete and authorize the engagement report on behalf of the firm for audit engagements, review engagements, all other assurance engagements, compilation engagements, and all certifications, declarations, and opinions referencing financial reporting standards. As outlined in clause 18(1)(a), 18(1)(b) and 18(1)(c) of the Act, this licence is issued when a member qualifies to practice in all the subcategories of the practice of professional accounting.

Specified Licence: A specified licence allows the member to complete and authorize the engagement report on behalf of the firm for review engagements, all other assurance engagements, compilation engagements, and all certifications, declarations, and opinions referencing financial reporting standards. As outlined in clauses 18(1)(b) and 18(1)(c) of the Act, this licence is issued when a member qualifies to practice professional accounting only in specified subcategories.

Compilation Licence: A compilation licence allows the member to complete and authorize the engagement report on behalf of the firm for compilation engagements. As outlined in clause 18(1)(c) of the Act, this licence is issued when a member qualifies to practice professional accounting in compilation engagements only.

Licence Application Process

Contact licensing if you require more information about the licensing application process and to obtain the application link and related forms.

For all licence types, there are 4 minimum qualifications necessary to fulfill on an initial licence application:

- Education

- Practical Experience

- Continuing Professional Development

- Competency Assessment (which includes a supervision component for assurance licences)

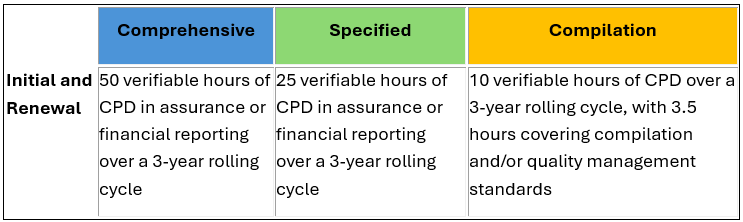

Summary requirements for an initial licence application for each licence type (details explaining each are outlined further below):

Comprehensive licence – to be able to issue all audit, review, other assurance, and compilation engagement reports and any other financial reporting opinions, certifications, or declarations, you must satisfy:

- Depth in the Assurance and Financial Reporting technical competencies within your professional education program.

- Minimum of 1,250 eligible practical experience hours, with at least 625 of those hours directly in audits of historical financial statements, over the past 5 years.

- A licensed professional accountant who holds at least equivalent licensure must have directly supervised your engagement work for at least two years in the past 5 years and will provide your competency assessment.

- Minimum of 50 continuing professional development hours over the last 3 years covering technical subject matter in assurance and/or financial reporting.

- A competency assessment provided by a licensed professional accountant who supervised your work as outlined above.

Specified licence – to be able to issue review, other assurance, and compilation engagement reports and any other financial reporting opinions, certifications, or declarations, you must satisfy:

- Depth in the Assurance and Financial Reporting technical competencies within your professional education program.

- Minimum of 1,250 eligible practical experience hours in assurance over the past 5 years.

- A licensed professional accountant who holds at least equivalent licensure must have directly supervised your engagement work for at least two years in the past 5 years and will provide your competency assessment.

- Minimum of 25 continuing professional development hours over the last 3 years covering technical subject matter in assurance and/or financial reporting.

- A competency assessment provided by a licensed professional accountant who supervised your work as outlined above.

Compilation licence – to be able to issue compilation engagement reports and any other financial reporting opinions, certifications, or declarations, you must satisfy:

- Depth in the Financial Reporting or Management Accounting technical competencies within your professional education program.

- Minimum of 15 completed compilation engagements over the past 5 years.

- Minimum of 10 continuing professional development hours over the last 3 years, with at least 3.5 CPD hours covering compilation and/or quality management technical subject matter.

- A competency assessment provided by a licensed professional accountant who holds at least equivalent licensure.

Detailed minimum licensing qualifications

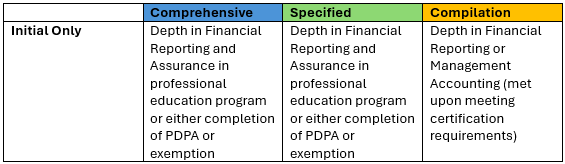

Education

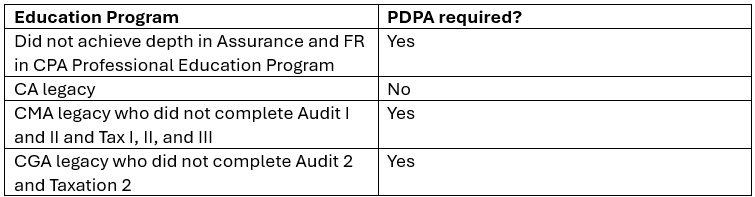

To qualify for a comprehensive or specified licence, a member must have obtained depth in the Assurance and Financial Reporting technical competencies (as outlined in the CPA Canada Competency Map) through their professional education program or must have completed the Post Designation Public Accounting (PDPA) program.

Applicants may be required to submit a copy of their transcript from a legacy education program.

To qualify for a compilation licence, a member must have obtained depth in either Financial Reporting or Management Accounting technical competencies (as outlined in the CPA Canada Competency Map), through their professional education program. For this license type, the education requirement is met upon meeting certification requirements and completion of the education program for any legacy program and the CPA Professional Education Program.

Members with a compilation licence expecting to practice in compilations reporting under a basis of accounting that will be under a general-purpose reporting framework within the CPA Canada Handbook should contact licensing prior to commencing the engagement for more information.

Post-Designation Public Accounting (PDPA) Program

The PDPA program is available to members in good standing who do not meet the education qualification for the assurance-based licences (comprehensive or specified). Members seeking a compilation licence are not required to complete PDPA. The PDPA program is available through the CPA Western School of Business. For more information on this program, click here.

Exemption available for several continuous years in practice at licensed firm in lieu of completion of PDPA

An exemption request may be available to the requirement to complete the PDPA in lieu of several years of continuous experience at a licensed firm. The applicant must submit the required request form which is reviewed and assessed for approval by the Professional Practice Committee at their next scheduled meeting. For more information on exemption requests see below or contact licensing.

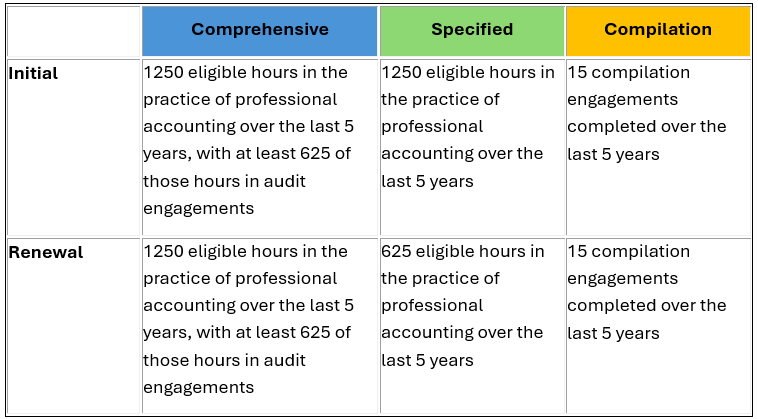

Practical Experience

All practical experience reported in a licence application must be accumulated and earned after becoming a member. Practical experience obtained as a candidate cannot be reported or will be disqualified in a licence application.

The practical experience for a comprehensive or specified licence is based on eligible hours earned by the member directly performing the engagement as part of the engagement team and may include a reasonable portion of time not charged to client engagements researching or analyzing assurance or financial reporting issues.

An eligible hour is defined in Rule 302.1(f) and is the time accumulated by a member in carrying out audits, reviews or other assurance and includes a reasonable portion of hours reported as unverifiable continuing professional development relevant to assurance or financial reporting matters.

Eligible hours do not include time accumulated by a member carrying out compilation engagements or any other regulated service[1]. Eligible hours cannot be reported in an application for time earned by other individuals.

The practical experience for a compilation licence is based on the number of completed compilation engagements under CSRS 4200. A completed engagement may be counted in each year for the same client. For example, an engagement completed for the same client in each of year for the past 5 years would count as 5 completed engagements.

Hours may be earned or engagements may be counted as completed when you are acting in any role on the engagement team (e.g., as engagement lead partner (once licensed), as a reviewer of the engagement work or completing the engagement work).

CPA Saskatchewan may request details and/or supporting documentation to be provided by a member for all practical experience reported at the time of application, renewal or during the firm's next practice inspection.

Exemption available for a shortfall in practical experience

An exemption request may be made by a licence applicant when there is a shortfall in eligible hours or number of completed engagements (as applicable based on the licence type) at the time of initial application or renewal. An exemption request cannot be made if the applicant has no (i.e. zero) relevant and recent practical experience to report. The applicant must submit the required request form which is reviewed and assessed for approval by the Professional Practice Committee at their next scheduled meeting. For further details on exemption requests, see below or you may contact licensing.

[1] Other regulated services include (as defined in Bylaw 2.1(v)): accounting services, bankruptcy and insolvency trusteeship or administration, engagement quality reviews, finance services, forensic accounting, management accounting or taxation services.

Continuing Professional Development (CPD)

Licensed members are required to take a prescribed amount of verifiable continuing professional development (CPD) hours specific to the practice of professional accounting to maintain their licence, as follows:

For comprehensive or specified licences, CPD must focus on applicable assurance, quality management or financial reporting topics within the practice of professional accounting. CPD covering subject matter in compilation engagements or taxation engagements cannot be allocated or will be disqualified for these licence types.

For a compilation licence, at least 3.5 CPD hours must relate to subject matter covering compilation engagement and quality management standards specifically. The remaining 6.5 CPD hours within the 3-year period may be in subject matter covering the taxation, management accounting or finance technical competencies. CPD that relates to enhancing professional judgement, critical-thinking skills, documentation skills, leadership skills or communication skills may be allocated within the portion of the 6.5 CPD hours. CPD relating to financial reporting standards may also qualify, provided it is relevant to the member's practice. For more information about licensing CPD, see our Guide to CPD Reporting.

CPA Saskatchewan may request supporting documentation be provided by a member for any or all CPD allocated to licensing in their CPD reporting at the time of application, renewal or during the firm’s next practice inspection.

CPD Plan available for shortfall in CPD hours

Where the minimum requirements for CPD are not met by the licence applicant at the time of initial application or renewal, the member may submit a CPD Plan for approval by the Registrar or Professional Practice Committee. For more information on CPD plans related to licensing, please contact licensing.

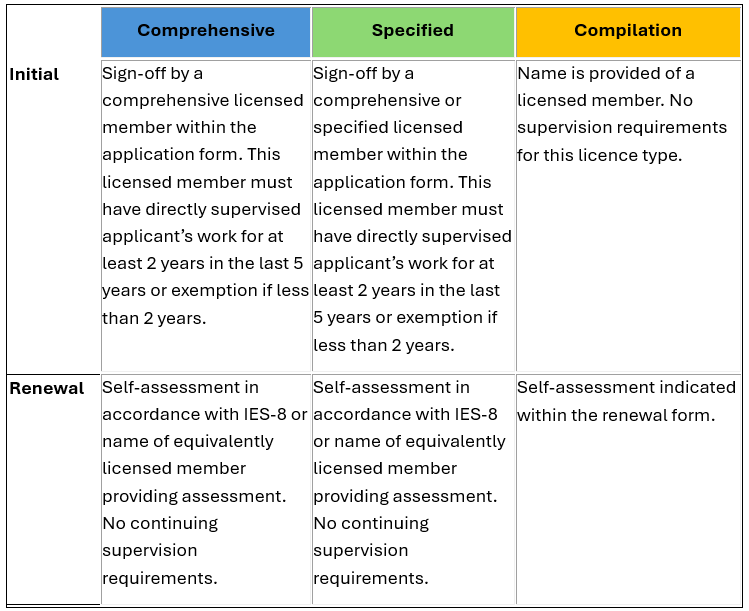

Supervision and Competency Assessment

For all licence types, upon initial application, a competency assessment is provided by a licensed member who holds at least an equivalent licence to the applicant and does not have a restriction for that licence type. The licensed member may be from any jurisdiction in Canada or Bermuda.

For comprehensive and specified licences, the licensed member providing the competency assessment must have directly supervised the applicant for at least two years within the last 5 years and must complete the applicable form that is provided with the application. The applicant may choose to also have the licensed member complete a form for the assessment based on the International Education Standard - IES 8 (note: the form is optional for use). For more information on the competency assessment form for a comprehensive or specified licence, please contact licensing.

Exemption available for a shortfall in supervision of 2 years

An exemption request may be made by a licence applicant when the applicant has been supervised by a licensed member for less than 2 years. An exemption request cannot be made if the applicant has not been directly supervised for any portion of the 2 years by the licensed member (i.e. zero). The applicant must submit the required request form which is reviewed and assessed for approval by the Professional Practice Committee at their next scheduled meeting. For further details on exemption requests, see below or you may contact licensing.

For an initial application for a compilation licence, there are no applicable forms or checklists that the licensed member is required to complete to provide the competency assessment. Instead, the licensed member must carry out the necessary steps, based on their professional judgement, to complete their due diligence to provide the assessment. Within the application, the member provides the name of the licensed member who has agreed to provide the assessment.

For all licence types upon renewal, a competency assessment may be provided by a licensed member or the member may complete a self-assessment. For comprehensive and specified licences, the self-assessment is based on the International Education Standard - IES 8.

CPA Saskatchewan may request supporting documentation be provided by a member for a competency assessment at the time of application, renewal or during the firm’s next practice inspection.

Exemptions, Conditions or Restrictions on a Licence

In accordance with the applicable Rules, the Professional Practice Committee may approve exemptions on a licence, may impose conditions on a licence, may place restrictions on a licence, or may cancel a licence for any matter other than those listed under Board Rule 333.19 and 333.20. These matters may include, but are not limited to practice inspection outcomes, non-compliance with a licence condition or restriction, or disciplinary matters.

Exemptions, conditions, or restrictions are listed on the member and/or firm’s licence and are accessible within the Portal. Conditions and restrictions are noted on the member and firm's publicly available status as ‘conditional’ or ‘restricted’. Further, restrictions are made publicly available on a named basis which includes a publication on our website for the member and/or firm. The Registrar may impose conditions on a licence and approve removal of licence restrictions.

Licence cancellations and restrictions are published in our firm newsletter and on our website.

For more information or if an application for licensing is required, please email licensing.